“New era of low interest rates” is often quoted as one of the main reasons for house price growth during 2000s. The argument claims that low interest rates reduce financing cost allowing house prices to increase for the financing cost reduction. This argument sounds very intuitive and as such it’s not questioned by many. So, let’s see how interest rates affect real (CPI adjusted) cost of house purchase.

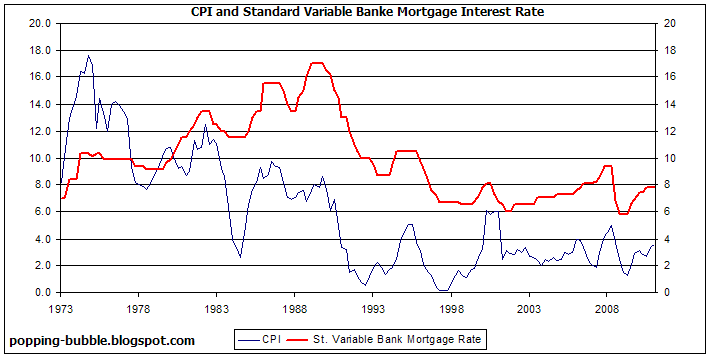

First of all we should check relation between CPI and mortgage interest rates. This relation will significantly affect real cost of mortgage. On Chart 1, we may see strong correlation between the two but we should also notice that ratio between mortgage interest rate and CPI is decreasing as CPI is getting higher. In other words the lower the CPI - banks are charging higher margin. This means that the lower CPI, the more (in real terms) mortgage holder pays to bank over the life time of the mortgage.

|

| Chart 1 - CPI and Standard Variable Bank Mortgage Rate |

To calculate cost of mortgage financing we developed Mortgage Interest Rate to CPI ratio - see Chart 2.

|

| Chart 2 - Annual CPI and Standard Variable Mortgage Interest Rate to CPI Ratio |

|

| Chart 3 - Standard Variable Mortgage Rate to CPI ratio vs. CPI |

When CPI is low banks are charging relatively (to CPI) high interest rates; on the other hand when CPI is extremely high banks charge less that CPI (they lose money). This combined with the fact that high inflation quickly reduces principal, should make us think that in real terms high CPI and higher mortgage rates could be better deal for mortgage holders. Chart 4 shows total cost of mortgage in CPI adjusted terms for 30 years 90% LVR loan for a given CPI and calculated interest rate based oh historic relation. Cost is calculated by assuming that CPI and interest rates remain the same over the entire period of the mortgage. This assumption is used to simulate cost dependency on low vs. high interest rate "eras" - argument used by people who claim that low Interest Rates (CPI) makes house purchase financing cheaper and house prices higher.

|

| Chart 4 - Total Real Mortgage Cost Index (30 year) |

Chart 4 shows that real cost of mortgage is significantly lower during periods of very high interest rates (high CPI). The reason for this is the fact that loan principal gets quickly eaten by inflation, and mortgage repayments quickly drop relative to income and other costs. It is also clear from the chart that cost of mortgage is relatively constant for periods when CPI is between 2 and 9%. So there are no reductions in total cost of financing house purchase between periods with moderate inflation (CPI 7-8%) e.g. during 1980s and periods with lower inflation (CPI ~3%) e.g. during 2000s.

Many people sell home before the end of the mortgage term so let's check what is the cost of mortgage for the first 10 years of 30 year mortgage - Chart 5. This period is selected because most of PPOR properties are held for at least 10 years before sale.

|

| Chart 5 - Real Mortgage Cost After the First 10 years |

As expected, cost of financing during first 10 years is higher for high interest rate mortgages, but unexpectedly for very high CPI periods cost decreases significantly. Cost of financing for the first 10 years is the highest for CPI around 8%. The difference between maximum cost for CPI of 7-8% (during 1980s) and cost for CPI of 3% (during 2000s) is around 20%. So if majority of people hold PPOR property for 10 years, cost of financing reduction due to low rates could drive prices 20% in real terms between 1980s to 2000s.

Lower interest rates also make repayments during first few years lower compared to income. This means that people can take much higher debt during low inflation periods if repayment as percentage of vs. income lending criteria remains the same.

|

| Chart 6 - Real Mortgage Cost Index |

From Chart 6. we may see that remaining part of a mortgage after 10 years is significantly lower during periods of higher inflation. This means that people much quickly repay their debts than what is the case for low inflation periods.

We may conclude that total cost of financing has general trend of falling with CPI and interest rate increase and it is fairly constant for low (3%) and medium (7%) CPI periods. As such, it cannot be used to justify real house price increase. Short term (10 year) mortgage cost is slightly lower during low inflation periods and could be used to justify house price increase of around 20%.

Most importantly lower interest rates make initial repayments lower allowing people to take much larger debt relative to income and that could be one of the key drivers (combined with lower LVRs) for house price increase during 2000s.

Low rates (CPI) allow people to take much more debt relative to income, they make mortgages more expensive over the mortgage life and they keep people in high debt for much longer period by keeping loan principal high. This is not only the key reasons why our (spending) economy is suffering but also the reason why it will not be able to recover anytime soon (if CPI remains on these levels).

To avoid this debt trap caused by low CPI and mortgage rates, banks could adjust lending criteria and take into account CPI levels. They had to reduce maximum LVR and maximum repayment relative to income to offset low interest rate trap. During 2000s, not only that we let low rates to do the damage but also our banks increased LVR and maximum repayments relative to income, creating huge debt problem that will cause economic pain for extended period.

Nice one.

ReplyDeleteHi,

ReplyDeleteMortgage interest rate is a useful tool that can save a home buyer considerable money in the long term. The sellers often make an offer to buy down interest rates as a way to attract buyers. Thanks a lot...

Sell Mortgage Note